3 Essential Steps to Building an Emergency Fund

A practical guide to creating and maintaining a robust emergency fund for unexpected expenses.

A practical guide to creating and maintaining a robust emergency fund for unexpected expenses.

3 Essential Steps to Building an Emergency Fund

Life is full of surprises, and while some are delightful, others can be financially devastating. That's where an emergency fund comes in – it's your financial safety net, a stash of cash specifically set aside to cover unexpected expenses without derailing your financial goals or plunging you into debt. Think of it as your personal financial superhero, ready to swoop in when life throws a curveball. Whether it's a sudden job loss, an unexpected medical bill, a car repair, or a leaky roof, having an emergency fund means you can tackle these challenges head-on, without stress-induced panic or resorting to high-interest credit cards.

For folks in the US and Southeast Asia, the importance of an emergency fund cannot be overstated. Economic landscapes can shift, and personal circumstances can change in an instant. Having this financial buffer provides peace of mind, allowing you to navigate uncertainties with confidence. It's not just about covering costs; it's about protecting your future investments, your credit score, and your overall financial well-being. So, let's dive into the three essential steps to building and maintaining a robust emergency fund that truly works for you.

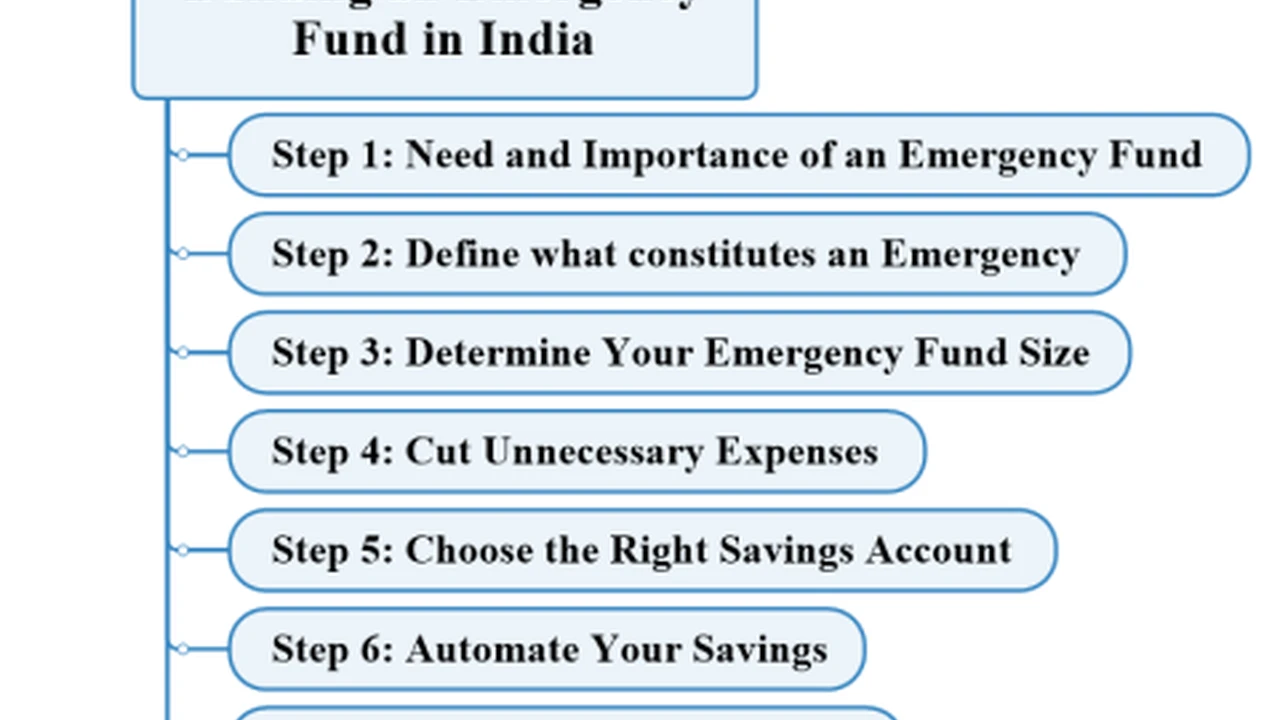

Step 1 Define Your Emergency Fund Goal How Much Do You Really Need

Before you start saving, you need a clear target. How much money should you aim to have in your emergency fund? The general rule of thumb is to save three to six months' worth of essential living expenses. However, this isn't a one-size-fits-all answer. Your ideal emergency fund size will depend on several factors, including your job security, health, family situation, and other financial obligations.

Assessing Your Monthly Essential Expenses Budgeting for Emergencies

First things first, you need to know your numbers. Grab a pen and paper, or open up a spreadsheet, and list all your truly essential monthly expenses. This isn't about your discretionary spending like dining out or entertainment; it's about the non-negotiables. Think:

- Housing: Rent or mortgage payments, property taxes, homeowner's insurance.

- Utilities: Electricity, water, gas, internet (often essential for work/communication).

- Food: Groceries, not restaurant meals.

- Transportation: Car payments, insurance, gas, public transport fares.

- Healthcare: Health insurance premiums, essential medications.

- Minimum Debt Payments: Student loan minimums, credit card minimums (though ideally, you'd pay more).

- Childcare: If applicable.

Add these up to get your total essential monthly expenses. Let's say this number comes out to $2,000. If you're aiming for three months, your target is $6,000. For six months, it's $12,000. Some financial experts even recommend up to 12 months for those with less stable income or significant health concerns.

Factors Influencing Your Emergency Fund Size Job Security Health and Dependents

Consider these points when setting your goal:

- Job Security: If you work in a volatile industry or your job isn't very secure, leaning towards the higher end (6+ months) is a smart move. If you have a very stable job with high demand, you might be comfortable with three months.

- Health: Do you or a family member have chronic health conditions that could lead to unexpected medical bills? A larger fund can provide peace of mind.

- Dependents: If you have children or other dependents, your financial responsibilities are higher, warranting a larger safety net.

- Other Income Sources: Do you have a side hustle or a partner's income that could help if your primary income stops? This might allow for a slightly smaller fund.

- Insurance Coverage: Good health, disability, and unemployment insurance can reduce the immediate need for a massive emergency fund, but it's still wise to have cash on hand for deductibles and waiting periods.

Once you have your target number, write it down. This concrete goal will motivate you throughout the saving process.

Step 2 Automate Your Savings Strategy and Account Selection

Building an emergency fund isn't about willpower; it's about automation and smart account choices. The easier you make it to save, and the harder it is to access for non-emergencies, the more successful you'll be.

Setting Up Automatic Transfers The Power of Pay Yourself First

The most effective way to save is to make it automatic. Treat your emergency fund contribution like any other bill. As soon as you get paid, have a set amount transferred directly from your checking account to your dedicated emergency fund savings account. This is the 'pay yourself first' principle in action.

- Frequency: Align transfers with your paychecks (weekly, bi-weekly, monthly).

- Amount: Start with what you can comfortably afford, even if it's a small amount. $25 or $50 a week adds up quickly. As your income increases or expenses decrease, increase your contribution.

- Consistency: The key is to be consistent. Even small, regular contributions will eventually reach your goal.

Many banks and financial institutions offer easy ways to set up recurring transfers online or through their mobile apps. Take advantage of these features.

Choosing the Right Account High Yield Savings Accounts vs Money Market Accounts

Where you keep your emergency fund is almost as important as how much you save. The ideal account should offer:

- Liquidity: Easy access to your money when you need it, without penalties.

- Safety: FDIC (US) or equivalent government insurance (e.g., PDIC in the Philippines, PIDM in Malaysia, SDIC in Singapore) to protect your deposits.

- Growth (modest): While not an investment, earning some interest helps your money keep pace with inflation.

High-Yield Savings Accounts (HYSAs)

These are often the best choice for emergency funds. They offer significantly higher interest rates than traditional savings accounts, sometimes 10-20 times more. They are typically offered by online banks, which have lower overheads and can pass those savings on to customers in the form of better rates.

- Pros: Higher interest rates, FDIC/government insured, easy online access, no monthly fees (usually).

- Cons: May not have physical branches (though this is rarely an issue for an emergency fund), sometimes have transfer limits (e.g., 6 withdrawals per month, though this is often waived for HYSAs).

Recommended Products (US Market):

- Ally Bank Online Savings Account: Consistently offers competitive rates, no monthly fees, 24/7 customer service, and easy online transfers.

- Discover Bank Online Savings Account: Another strong contender with good rates, no fees, and excellent customer service.

- Marcus by Goldman Sachs Online Savings Account: Known for competitive rates and a straightforward user experience.

- Capital One 360 Performance Savings: Good rates, no fees, and integrates well if you already bank with Capital One.

Recommended Products (Southeast Asia Market - examples, rates vary by country and time):

- Singapore: DBS Multiplier Account (requires meeting certain criteria for higher rates), OCBC 360 Account (similar criteria). For simpler HYSAs, consider CIMB FastSaver.

- Malaysia: Maybank Islamic Ikhwan Savings Account-i (often has promotional rates), CIMB e-Account.

- Philippines: ING Savings Account (online-only, often competitive rates), CIMB Bank PH Savings Account (online-only).

- Thailand: TMB All Free Account (often has higher interest tiers), KBank K-eSavings Account.

- Indonesia: Jenius by BTPN (digital bank with competitive rates), Bank Jago (another popular digital bank).

Money Market Accounts (MMAs)

MMAs are similar to HYSAs but sometimes come with check-writing privileges and debit cards. They might offer slightly lower interest rates than the top HYSAs but can be a good option if you want a bit more flexibility in accessing your funds directly.

- Pros: Often higher rates than traditional savings, check-writing/debit card access, FDIC/government insured.

- Cons: May require a higher minimum balance to open or avoid fees, rates can sometimes be lower than HYSAs.

Comparison: For most people, a High-Yield Savings Account is the superior choice for an emergency fund due to typically better rates and the psychological barrier of not having immediate debit card access, which helps prevent impulse spending from your emergency stash. The goal is to make it accessible for emergencies, but not too easy for everyday wants.

Step 3 Replenish and Review Your Emergency Fund Regularly

Building your emergency fund is a fantastic achievement, but it's not a one-and-done task. It requires ongoing maintenance, just like any other important financial asset.

Using Your Emergency Fund When Disaster Strikes How to Access Funds

The whole point of an emergency fund is to use it when a true emergency arises. What constitutes an emergency? It's an unexpected, necessary expense that you cannot cover with your regular income or other savings without going into debt. Examples include:

- Job loss or significant income reduction.

- Major unexpected medical expenses (after insurance).

- Essential home repairs (e.g., furnace breakdown, burst pipe).

- Major car repairs that prevent you from getting to work.

- Unforeseen travel for a family emergency.

It is NOT for:

- A new gadget you really want.

- A spontaneous vacation.

- Holiday shopping.

- A down payment on a house (that's a separate savings goal).

When an emergency hits, access your funds from your chosen high-yield savings or money market account. Transfers to your checking account usually take 1-3 business days, so plan accordingly if it's an immediate need. For very urgent situations, some online banks offer expedited transfers or wire transfers for a fee.

Rebuilding Your Fund After Use Strategies for Quick Replenishment

Once you've tapped into your emergency fund, your next priority should be to replenish it. Think of it like refilling your car's gas tank after a long trip. You don't want to be caught with an empty tank for the next journey.

- Prioritize Replenishment: Make refilling your emergency fund your top financial goal, even above other savings or debt repayment (except high-interest credit card debt).

- Increase Contributions: Temporarily increase your automatic transfers until the fund is back to its target level.

- Cut Discretionary Spending: Temporarily reduce non-essential expenses like dining out, entertainment, or subscriptions to free up more cash for saving.

- Find Extra Income: Consider a temporary side hustle, selling unused items, or taking on extra shifts to boost your income and accelerate replenishment.

- Windfalls: If you receive a bonus, tax refund, or unexpected gift, direct a significant portion (or all) of it to your emergency fund.

Annual Review and Adjustment Keeping Your Fund Relevant

Your financial life isn't static, so your emergency fund shouldn't be either. Make it a habit to review your emergency fund at least once a year, or whenever there's a significant life change.

- Recalculate Expenses: Have your essential monthly expenses increased due to inflation, a new car, or a growing family? Adjust your target fund size accordingly.

- Life Changes: Did you get a new job with less security? Did you buy a house? Did your health situation change? These events might warrant increasing your fund.

- Interest Rates: Check if your high-yield savings account is still offering competitive rates. If not, consider moving your funds to an account with a better return.

- Investment Goals: As your emergency fund grows, you might find you have excess cash beyond your emergency needs. This is a great problem to have! You can then consider moving those extra funds into investment vehicles for long-term growth, but always ensure your core emergency fund remains intact and separate.

Building an emergency fund is one of the most fundamental and empowering steps you can take for your financial health. It's not just about money; it's about peace of mind, resilience, and the freedom to make choices without being dictated by unexpected financial pressures. Start today, even if it's with a small amount, and watch your financial confidence grow.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)